What Is Debt Recycling? A Plain-English Guide for Australian Homeowners

What Is Debt Recycling?

Debt recycling is one of the most powerful — and most misunderstood — wealth-building strategies available to Australian homeowners. Done correctly, it can turn your non-deductible home loan into a tax-effective investment vehicle, accelerate your path to financial freedom, and build a significant investment portfolio alongside your mortgage repayments.

But it's not for everyone. And it's not as complicated as it sounds. Let me break it down in plain English.

The Core Concept

Your home loan interest is not tax deductible — the ATO doesn't allow you to claim interest on money borrowed to buy your own home. But interest on money borrowed to invest in income-producing assets (like shares or managed funds) is tax deductible.

Debt recycling is the process of converting your non-deductible home loan debt into deductible investment debt — gradually, over time, using your own equity.

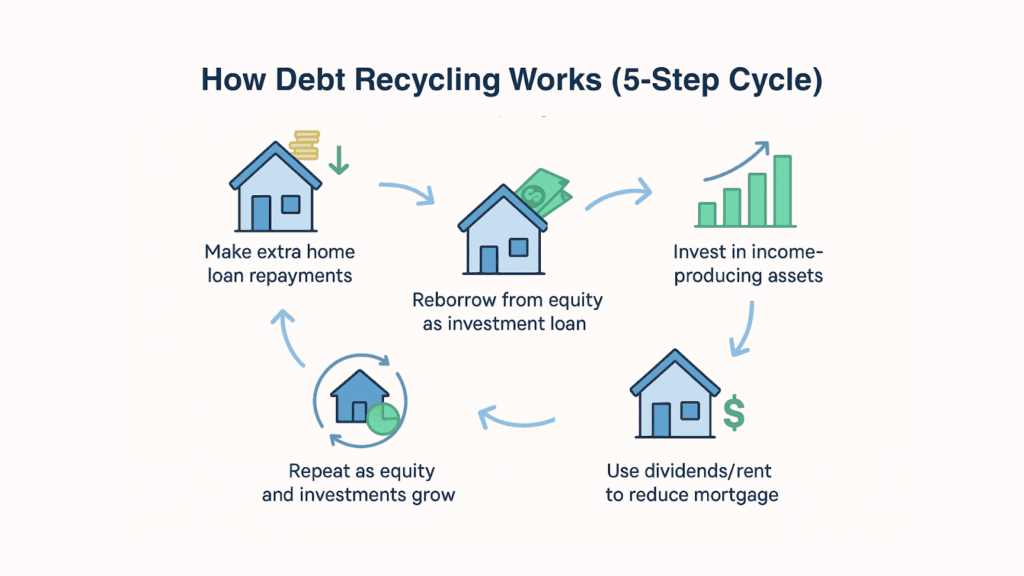

How It Works — Step by Step

- Make extra repayments on your home loan. Every dollar you pay down above your minimum repayment builds equity in your home.

- Access that equity via a split loan or line of credit. Once you've built equity, you redraw it (or draw from a separate investment loan facility) and invest it into income-producing assets — typically a diversified share portfolio or ETFs.

- Use the investment income to make more home loan repayments. Dividends and distributions from your investments go straight back onto your home loan, building more equity faster.

- Repeat the cycle. As you pay down more of your home loan, you access more equity, invest more, and the cycle accelerates.

- Claim the interest as a tax deduction. The interest on the investment portion of your debt is tax deductible, reducing your taxable income each year.

A Simple Example

Let's say you have a $500,000 home loan and you make $20,000 in extra repayments over the year. You then redraw that $20,000 and invest it into a diversified ETF portfolio. The interest on that $20,000 investment loan is now tax deductible.

If your investment earns $1,000 in dividends, that goes back onto your home loan. You then redraw again and invest again. Over 10–15 years, this cycle can result in a substantial investment portfolio — built largely from equity you already had — while simultaneously paying off your home loan faster.

The Tax Advantage

The real power of debt recycling is the tax deduction. If you're on a 37% marginal tax rate and you're paying $10,000 per year in investment loan interest, you get $3,700 back at tax time. That's money that would have gone to the ATO, now going toward your wealth.

Over 10–20 years, the compounding effect of this tax saving — reinvested into your portfolio — can be significant.

Who Is Debt Recycling Right For?

Debt recycling works best for people who:

- Own their home (or have significant equity — typically 20%+ in their property)

- Have a stable income and can comfortably service both their home loan and investment loan

- Have a long investment time horizon (10+ years)

- Are comfortable with investment risk — your portfolio will go up and down

- Are in a higher marginal tax bracket (the higher your tax rate, the bigger the deduction benefit)

The Risks — Be Honest With Yourself

Debt recycling is not a get-rich-quick strategy. It involves borrowing to invest, which amplifies both gains and losses. If your investments fall in value, you still owe the debt. If interest rates rise, your repayments increase. If your income drops, you need to be able to service both loans.

The key risks to understand:

- Investment risk: Markets go down. Your portfolio could lose value in the short term.

- Interest rate risk: Rising rates increase your loan repayments.

- Liquidity risk: Your wealth is tied up in property and investments — not easily accessible in an emergency.

- Complexity risk: Getting the structure wrong can cost you the tax deduction entirely. This is why professional advice matters.

Getting the Structure Right

The ATO is very specific about what qualifies as a tax-deductible investment loan. The most important rule: the borrowed money must go directly into income-producing investments. It cannot pass through your offset account or be mixed with personal funds.

This is where many people get it wrong — and why working with a qualified financial planner is essential. The loan structure, the investment selection, and the documentation all need to be set up correctly from day one.

Debt Recycling vs. Negative Gearing

These two strategies are often confused. Negative gearing is when your investment costs (including interest) exceed your investment income — creating a tax loss you can offset against your salary. Debt recycling can be negatively geared, but it doesn't have to be. Many debt recycling strategies use positively geared or neutral investments.

The key difference: debt recycling is a process (converting non-deductible debt to deductible debt), while negative gearing is an outcome (your investment runs at a loss for tax purposes).

Is Debt Recycling Right for You?

If you own your home, have stable income, and are thinking long-term about building wealth — debt recycling is worth exploring. It's not a strategy you set up in an afternoon, but with the right structure and professional guidance, it can meaningfully accelerate your path to financial freedom.

If you'd like to explore whether debt recycling is right for your situation, book a free 15-minute strategy call with me. We'll look at your numbers, your goals, and whether this strategy fits your financial picture.

This article is general information only and does not constitute personal financial advice. Please consult a qualified financial adviser before implementing any investment strategy.

About Jessie Culgan

Jessie Culgan is a qualified financial planner and the founder of Culgan Wealth. With years of experience helping Australian women build real, lasting wealth, Jessie created Culgan Wealth to make professional financial education accessible to everyone. Real money. Real talk.

General Advice Disclaimer: The information in this article is general in nature and does not take into account your personal financial situation, objectives, or needs. It is provided for educational purposes only and does not constitute personal financial advice. For advice tailored to your circumstances, please consult a qualified financial adviser or contact Jessie at culganwealth.com.au.

Jessie is a qualified financial planner and certified technical analyst with 8+ years of experience across ASX equities, US markets, and superannuation. She built Culgan Wealth to make real financial education accessible to everyday Australians — no jargon, no fluff.

Join the Community — It's Free